When BC Hydro said that growing demand required asset additions worth billions of dollars and contractual commitments of $50+ billion owed to independent power producers, should we have believed what they said? The record clearly states the answer was NO.

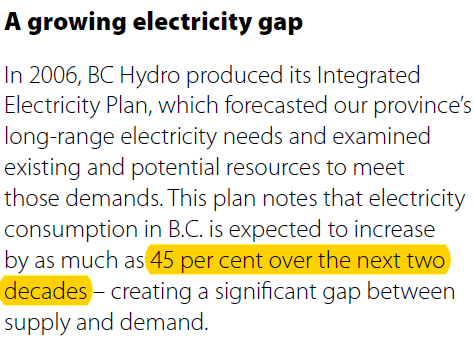

Here is the utility’s demand forecast from a document titled Peace River Site C Hydro Project published when the new dam was being promoted (emphasis added):

Data in BC Hydro’s Annual Reports allow us to chart actual demand growth from fiscal year 2006 to fiscal year 2023. The chart below forecasts 1.88 percent growth each year, a figure that would produce 45 percent demand growth over two decades.

With the Site C construction project said to end by 2025, BC Hydro is selling a new bill of goods to keep the empire expanding. This year it announced that demand will grow 15 percent by 2030. The company’s apparent aim is to issue yet more electricity purchase contracts to IPPs.

We have not seen a revision to the $16 billion Site C budget since February 2021. At that time, the Trans Mountain Pipeline expansion budget was $12.6 billion. Two years later, the TMX budget had swollen to $30.9 billion. When the final Site C budget is known, expect another shock.

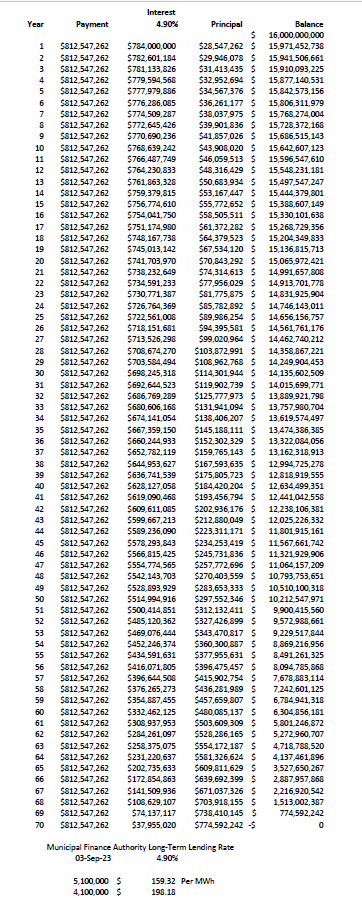

The Municipal Finance Authority currently reports long-term interest at 4.90 percent. At that rate, BC Hydro would have to pay $812.5 million each year to retire a $16 billion debt in 70 years. If Site C produces 5,100 GWh as promised, that is an annual capital commitment of $160 per MWh. If a year’s production is only 4,100 GWh, as suggested in this earlier In-Sights article, the commitment rises to $200 per MWh.

Operating, administrative, and distribution costs must be added to determine the cost of Site C power, so $200 MWh may be conservative. BC Hydro’s sales revenue from residential, commercial and industrial customers averaged $92.55/MWh in the fiscal year just reported but LNG producers are promised electricity at about 2/3 of that average price.

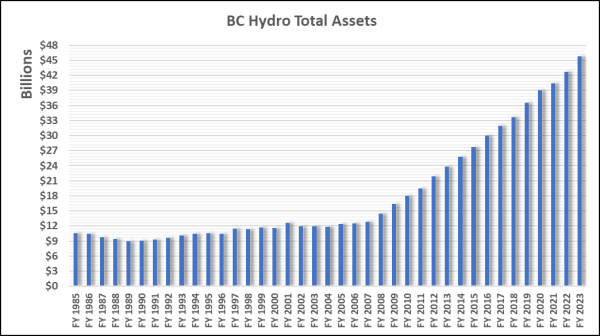

Note that BC Hydro’s total assets grew slowly when demand was rising, but when sales to domestic consumers flatlined, asset growth surged.

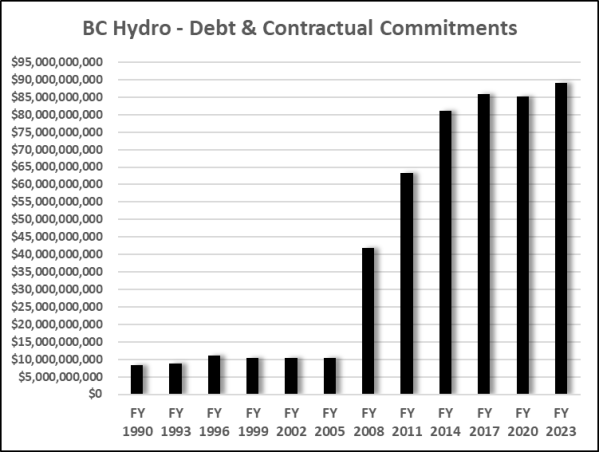

However, the chart of total assets is incomplete because BC Hydro has commitments for private power that obliges the company to pay more than $50 billion in future IPP payments. This chart accounts for both direct debts and contractual commitments.

After years of close observation, I remain convinced that BC Hydro has been a disaster for consumers and taxpayers. However, it has been a sweet deal for those seated in the company’s boardrooms.

Were legacy media still engaged in public interest journalism, the information here would be front page news.

Who believes BC Hydro? Well I certainly don’t.

Fact is, I do not believe any senior bureaucrat in BC or Canada.

Bureaucrats today are unabashed liars and grifters have conned their up the bureaucratic food chain.

It is the Peter Principle on steroids.

LikeLike

Hi Norman, can you clear up for me where your numbers come from concerning Hydros costs to pay off Site C? At 4.9% and 16 Billion I get interest charges of 784 million per year, and then an averaged out principle payout of another 228 and a half million per year makes for a little over a billion per year.

Randy

LikeLike

Thanks for asking, I welcome requests for clarification when an assertion is published here.

I calculated blended payments of principal and interest on a spreadsheet. An image showing the calculations has been added to the article.

LikeLiked by 1 person

Norm,

Update your prices to $160/MWh and $200/MWh (as shown in your spreadsheet)

Have you read the Information Requests in the BCUC IRP? The interveners don’t believe BC Hydro either

LikeLike

Indeed, corrected now.

LikeLike

Looks like we ratepayers are going to be in debt forever not to mention the long term damage to the environment from this dam – damage that extends all the way to the Arctic ocean.

LikeLike

when is the govt going to take over BC Hydro and run it as a reliable business

LikeLike

The gov’t has ALWAYS controlled BC Hydro. The political interference is why it is not run as a reliable business. Hydro executives have to be puppets of the gov’t; otherwise they are gone.

Burrard Thermal should have been retained as a standby plant for emergencies, but the BC Liberals forced Hydro to shut it down, bypassing the BCUC.

Site C had no business case and was fraught with geotechnical perils, but the Liberals forced Hydro to build it anyway, again bypassing the BCUC. Site C’s power will cost $200+ per MWh, while the market rate is $40/MWh. It is a money pit.

LikeLike

People should know that Martin Cavin is a former power engineer and manager at Burrard Thermal. He knows whereof he speaks.

LikeLike

Does BChydro bypass power production (spill),at times, to fulfill p3 contracts- ergo a level 2 provider?

Did/does burrard thermal output come close to site C?

is there a webpage showing p3 power contract expiry dates.?

LikeLike

BC Hydro makes no admission about generating less power than their generating equipment permits, but there is direct and indirect evidence this is correct.

Burrard Thermal’s capacity was 950 MW, so much like that planned for Site Cecrecy.

Beyond naming the IPP contractors, BC Hydro’s deals for private power are secret. That is an appalling situation when almost 1.5 billion dollars a year of public money is given to private companies that are mostly owned outside the province.

LikeLike